September 6, 2019 / 07:35

In the 2Q2019, the Agora Group once again increased its revenues. The inflows grew in all major business lines of the Group. The sharpest increase occurred in revenues from cinema operations resulting from the double-digit dynamics of tickets sales in Helios network, which outperformed the cinema market’s one. Additionally, Agora noted an increase in copy sales revenues and at the same time strengthened its position in the area of outdoor advertising – due to AMS’ advertising income growing faster than OOH market as well as acquisition in the digital out-of-home segment.

The results of the Agora Group in 2Q2019 were significantly impacted by the entry into force of IFRS 16. In order to maintain the comparability of data, this press release presents data without the impact of IFRS 16. More information on the effects of implementing IFRS by the Agora Group can be found in the financial statements for 2Q2019.

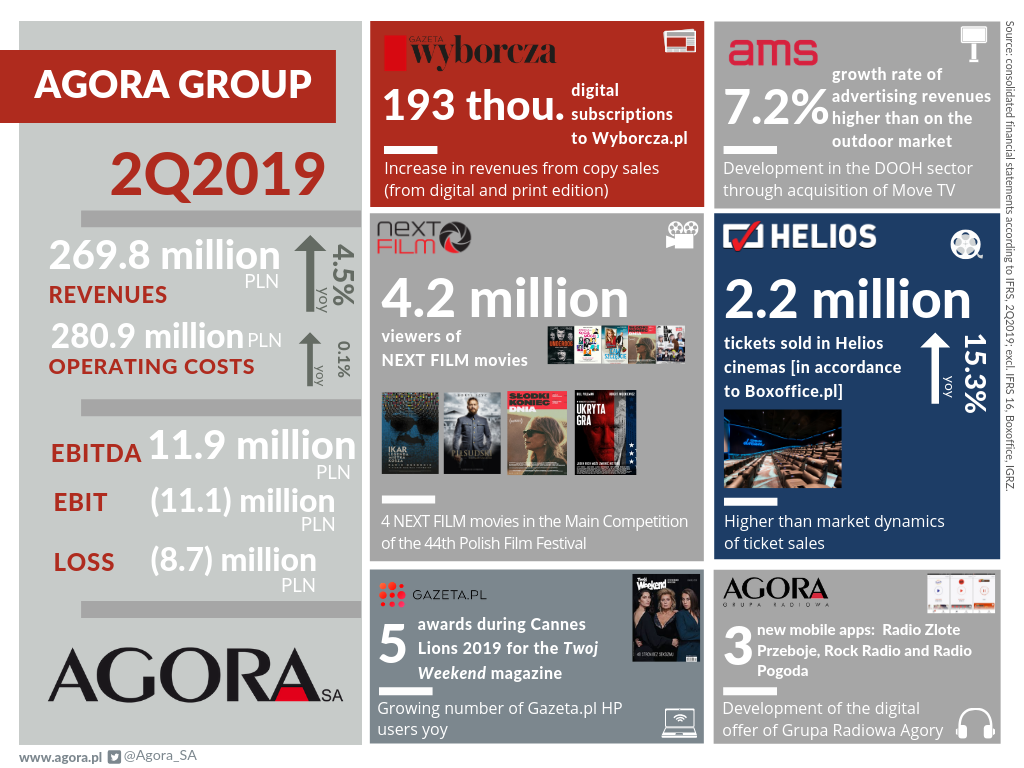

In 2Q2019, total revenues of the Agora Group increased by 4.5% yoy and amounted to PLN 269.8 million. This resulted from the increase in all income categories except for those from the printing activity. The largest impact on the Group's results had again the growing inflows of the Helios network, which recorded an increase in revenues from cinema tickets sales by 12.0% to PLN 39.2 million and from concession sales - by as much as 29.7% to PLN 17.9 million. Such results of cinema business were ensured primarily by higher than the market attendance growth dynamics in Helios multiplexes - over 2.1 million tickets were purchased in these cinemas in the discussed period (up by 14.5%), while the total number of tickets sold in Polish cinemas grew by 1.7%1. The increase in revenues from the copy sales of Agora Publishing House and of Gazeta Wyborcza - both from subscriptions to Wyborcza.pl and paper edition of the daily - translated into a significant, 12% rise in the Group's income from the copy sales. Inflows from other sales also increased, mainly owing to the first revenues from restaurant business. Advertising revenues were slightly higher, out of which the income of the Outdoor segment increased the most, particularly due to the campaigns carried out on Premium Citylight and Digital panels, as well as that of the Internet segment - due to a significant increase in Yieldbird's revenues. The only decline was recorded in revenues from printing services resulting from a lower volume of orders, especially in the coldset technology.

The Agora Group's net operating costs in 2Q2019 [excluding IFRS 16] decreased to PLN 280.9 million yoy. Among various categories of expenditure, the most significant were costs of external services, which grew by 8.5% to PLN 109.5 million, primarily due to the increase in expenditure in cinema, restaurant and movie business, as well as higher costs of lease of advertising space in the Internet segment. The staff costs, higher by 5.4% yoy, increased in all Group’s segments except for the Press and Internet. Almost a 12% upturn in D&A costs resulted mainly from higher expenditure in the Movies and Books, Print and Internet segments – in connection with: higher number of cinemas in Helios network, accelerated depreciation of machinery in closed printing plants, and investments in online activity, respectivelly. Additionally, Agora Group noted also an increase in costs of materials and energy consumed and the value of goods and materials sold, as well as a slight growth in expenditure on marketing and promotion.

The Group’s headcount at the end of June 2019 was 2,628 FTEs, having decreased by 148 FTEs yoy. This decline resulted mainly from lower level of employment in the Press, Internet, Print and Outdoor segments, as well as in supporting divisions.

It is noteworthy that several events influenced the comparability of Agora Group's results in 2Q2019 with the same period of 2018. In the 2Q2018, the level of the Group's operating costs was negatively affected by: an impairment loss on receivables at risk of uncollectability from RUCH S.A. in the amount of PLN 15.7 million and restructuring provision in the Press segment in the amount of PLN 2.2 million. On the other hand, the sale of Stopklatka S.A. shares had a positive effect on the net result of the Group.

As a result, in 2Q2019, the Agora Group recorded profit at EBITDA level excluding IFRS 16 in the amount of PLN 11.9 million. The loss at the EBIT level excluding IFRS 16 stood at PLN 11.1 million, while the net loss excluding IFRS 16 amounted to PLN 8.7 million. The net loss attributable to equity holders of the parent company excluding IFRS 16 accounted for PLN 8.4 million.

According to IFRS 16, the Group’s EBITDA was positive and amounted to PLN 30.1 million. The operating loss at the EBIT level amounted to PLN 9.2 million and the net loss to PLN 6.6 million. The net loss attributable to equity holders of the parent company stood at PLN 6.3 million. What is important, exchange rate differences resulting from implementation of IFRS 16 had a positive impact on the Group ‘s net result.

The Agora Group successfully implements subsequent projects in line with the its business strategy for 2018-2022, including those related to sales of content in the subscription model. One of the main factors ensuring the growth of copy sales revenues in the Press segment in 2Q2019 was an increase in inflows from digital subscriptions. The number of active subscriptions to Wyborcza.pl content at the end of June this year, amounted to 193 thousand. In combination with the average distribution of the paper issue at the level of 101 thousand copies, this means an average of over 290 thousand daily accesses to the content of Gazeta Wyborcza.

The Agora Group is also expanding its operations on prospective markets. Yieldbird continued this year's development of international activities, primarily by acquiring customers in the United States, Denmark, Ireland and Serbia, as well as establishing partnerships in Brazil and the Nordic countries. Agora increased also its involvement in ROI Hunter, acquiring more shares of the company and accumulating them to almost 24% as part of the second round of financing.

In July 2019, AMS finalized an acquisition in the digital out-of-home (DOOH) segment, becoming the majority shareholder of the Piano Group, an operator of a MoveTV platform with screens in the largest fitness clubs in Poland and premium content adapted to watching during training. Thanks to this transaction, Move TV will join the AMS digital portfolio, strengthening the company's position on the rapidly growing DOOH market.

There are currently 14 eateries under the Papa Diego brand and 4 under the Van Dog brand, managed by the Helios network Additionally, due to Helios’ collaboration with some of the partners of the Food for Nation company, the owner of the Pasibus burger chain, there are already 3 restaurants opened under this brand. Further openings are planned for 4Q2019.

Data source: consolidated financial statements according to IFRS, 1H2019.

Footnotes:

1 Attendance data at Helios cinemas is reported in accordance with calendar periods, while market attendance data - according to Boxoffice.pl. In the latter approach, the sale of cinema tickets is reported in periods that are not identical to the calendar month, quarter or year. The number of tickets sold in a given period is measured from the first Friday of a given month, quarter or year to the first Thursday in the following month, quarter or reporting year.

In terms of Boxoffice.pl data, Helios's results in the discussed period would be even better - the number of tickets sold would increase by 15.3% to 2.2 million.

Go back